This one should be short and sweet, it’s really just a brain dump of a conversation I had with a friend who had the all too common argument of ‘But It’s so expensive, I can’t afford R9500 payments’. It’s the same excuse I used for years, but it’s only semi true.

Housing is a commodity. All commodities are subject to supply and demand economics. There are millions of people who would love to buy a house and only a few houses.

Supply and demand says that when there is high demand and limited supply, prices go up… not everyone understands why though.

Think of an auction: The audience is made up of an accurate cross section of South African society. 90% of them earn less than R5000 a month. 5% earn around R10 000 a month. 3% earn around R20 000 a month, 1% earn around R35 000 a month and the other 1% earn more than R45 000 a month.

(I made those stats up because the StatsSA release is so racially oriented I was unable to find a non-race income breakdown. If anyone knows of better percentages I’d love to see them)

Ok, so we’re at this auction and there are 98% of the people earn less than R20 000 a month… and there’s only 3 houses for sale. That last 2% will outbid anyone in the other 98%, but they’ll stop when it starts hurting…. the housing price is therefore completely linked to the salaries of the highest income earners in the country. Now, people like my friend and I are lucky to be in or near that top 3% but we certainly aren’t that top 1%. Which means that whenever we want to buy there will be some fatcat pushing the price up… but with some belt tightening, we’ll be able to afford it.

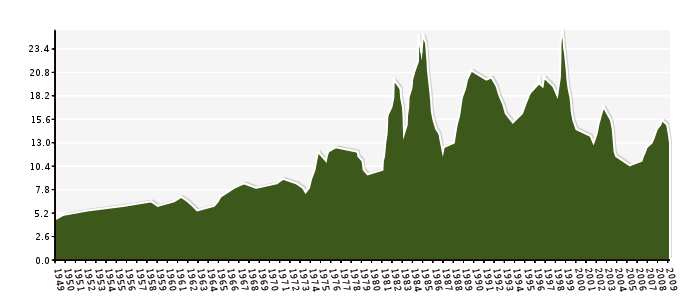

Ask an older friend who bought property about their bond repayments… I know guys who are paying R950 every month towards their bond. The natural instinct is to say ‘Oh man, I wish I’d bought when the prices were still so low”, but the truth is, the prices were never low. My parents had to pay R120 bond payments when they first bough their house 29 years ago. They struggled. My mom says there was a time when the stopped buying cheese because it was a luxury!

It all boils down to this. Unless you are earning a salary in the top 1% of the population, it is going to hurt a little bit when you buy property. But soon enough salaries will go up and your bond payment will stay R9500 a month. I just know that one day, in the hopefully not too distant future, someone will say ‘Oh man I wish I had bought property when the payments were still under R10 000’.

(I realise that this summary completely ignores cheaper housing in cheaper areas, but I did that to keep it simple)

ps. Analysts predict that the housing price will skyrocket in 2010… but there’s a chance (Skye, block your ears) that we might be in for another percent increase in prime during August. Eek!

A few months ago, before we had moved into our new house, I decided that one of the small things I couldn’t wait to do was to install a knife rack.

A few months ago, before we had moved into our new house, I decided that one of the small things I couldn’t wait to do was to install a knife rack. Be sure to read the overly long winded “

Be sure to read the overly long winded “